Credit to Alex Fakhre for coining the term "AI rapture" as an elegant alternative to the more mainstream “Saaspocalypse”. Whatever you call it, founders, VCs, and tech investors are anxious right now. Who will be the chosen ones? Who will be worth nothing after ten years of 120-hour weeks on a meager salary?

The anxiety is not unfounded. Public SaaS multiples have been contracting sharply, and the obvious question for any founder sitting on a software business is whether this is temporary noise or something structurally different. The short answer: it is some of both. But the nuance matters a great deal depending on what kind of SaaS you have built.

In this article, I walk through what I am seeing in the data (public and private) and lay out a framework for SaaS founders in the mid-market to think about which businesses are genuinely at risk from AI disruption, and which ones are not.

SaaS valuations in 2026: what the multiple data shows

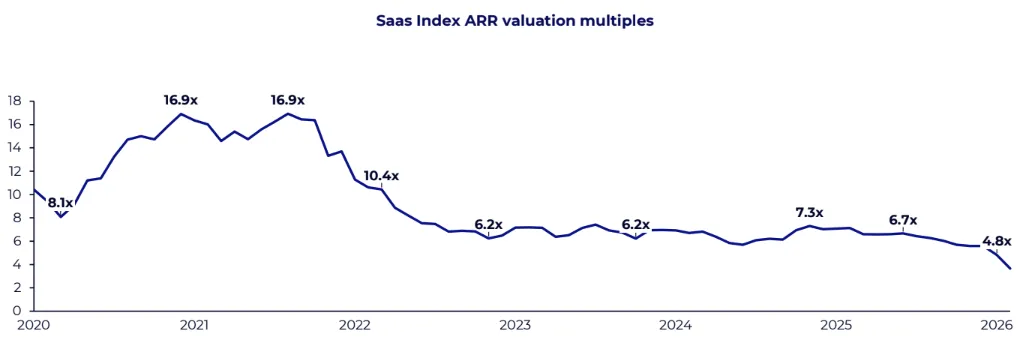

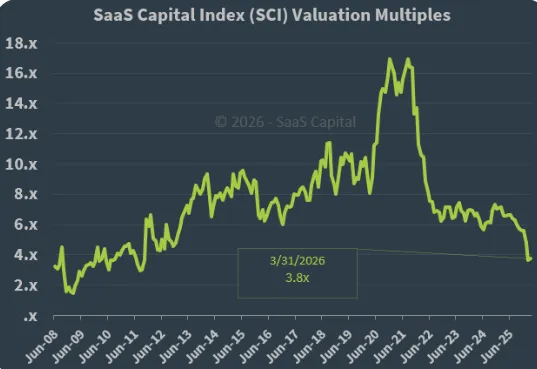

The chart below tells a clear story. The SaaS Capital Index peaked at 16.9x ARR in 2021, compressed hard through 2022 and 2023, and appeared to stabilize around 6-7x through most of 2024 and into early 2025. Then it resumed its fall. By March 2026, the index stood at 3.8x. There is no ambiguity about the direction.

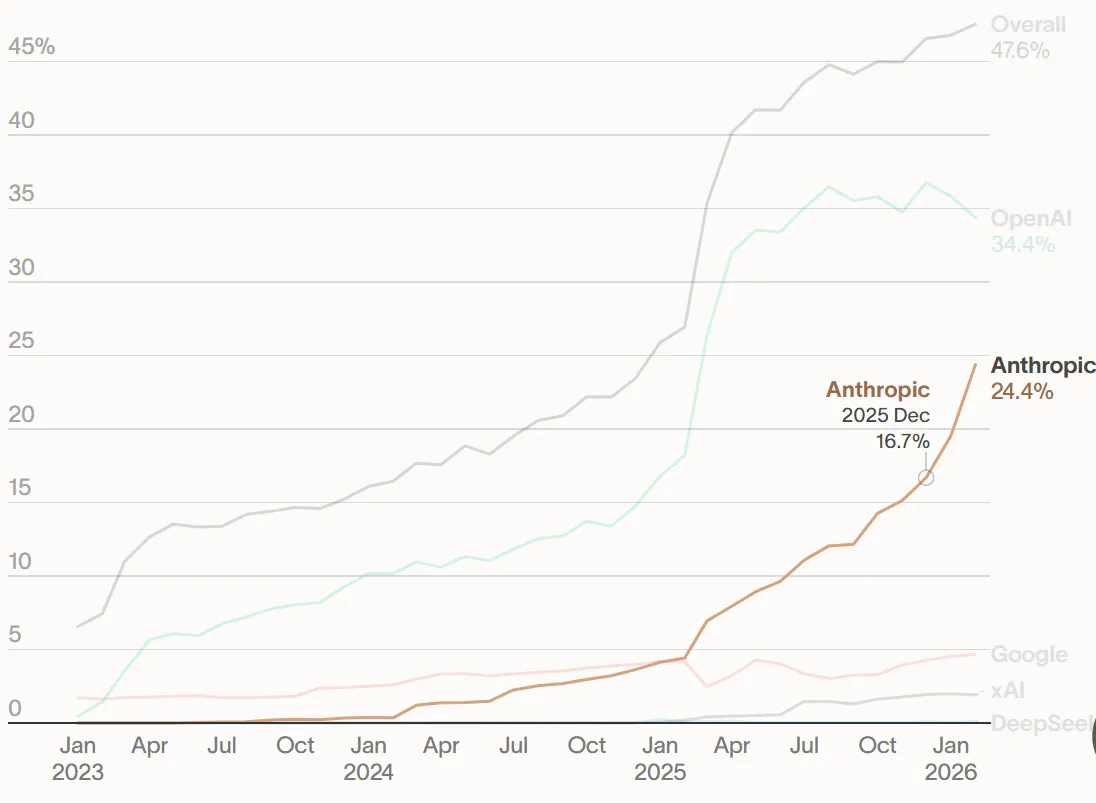

What drove the acceleration after mid-2025? This second chart below, from Ramp's AI spend index, which tracks market share across AI providers, tells a parallel story. The two data series are negatively correlated. As AI spending, and more importantly, AI capability, accelerated; SaaS multiples moved in the opposite direction.

Nobody was really worried when the first wave of generative AI produced conversational chatbots and slop images. What changed investor sentiment was the rollout of reasoning models and coding agents as tools that can autonomously execute multi-step software workflows. That is a different threat vector than a better search box, and that’s what we’re seeing reflected in SaaS valuations 2026.

Will AI hurt my SaaS valuation? Not all is made equal

The aggregate multiple compression obscures a more interesting story underneath. Zoom in on individual companies and the dispersion is striking.

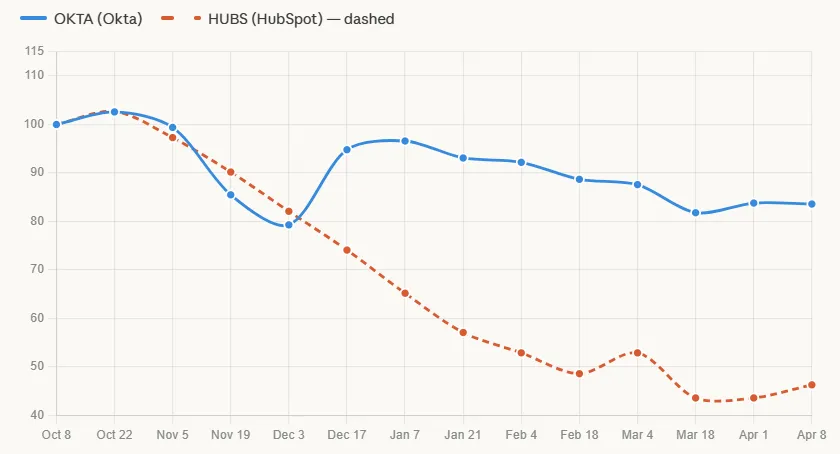

HubSpot lost more than half its market cap in the six months to April 2026. Okta declined roughly 16% over the same period. That is not a rounding difference. It signals that the market is making a distinction between SaaS companies where AI can plausibly replicate the core function, and SaaS companies where it cannot.

Martech and CRM platforms face a genuine substitution question: if a sufficiently capable AI agent can manage customer relationships and marketing workflows directly, what is the incumbent software worth? Security platforms face a different question. Identity, access management, and compliance are not tasks you hand to a general-purpose AI agent. The regulatory and operational requirements create a moat that is harder to erode.

Are 2026 SaaS multiples actually low? A reality check

Let’s zoom out too. Before panic sets in, some historical context is useful. A 4x ARR multiple, with a typical SaaS EBITDA margin of around 10%, implies investors are discounting more than 40 years of steady future cash flows, or expecting significant near-term growth. On that math, maybe HubSpot was never worth 7x ARR to begin with, regardless of AI.

Zoom out even further and the picture gets more grounding. The chart below shows the SaaS Capital Index going back to 2008. The high-multiple environment of 2013-2025 looks, in retrospect, like the anomaly. Rates were at zero. Growth was valued above everything else. The 2020-2021 spike was extreme even by the standards of that era. What the market is currently repricing may not be the value of software businesses, but the inflated expectations that cheap money created.

What is really happening in private SaaS M&A markets

Private deal flow and valuations remain robust for now. There is typically a 6-12 month lag between public multiple movements and private market pricing. This is because private deals take time to negotiate, and sellers are slower to reprice expectations than public markets. That lag is real and it creates a window, though it is not permanent. The recent tightening in private credit markets will have some impact on valuations over time, though equity-focused tech funds do not rely heavily on leverage in their acquisitions, so the effect is more moderate than in buyout-heavy sectors.

Private equity dry powder globally remains substantial at approximately two trillion dollars, and there is no sign that deal volume is collapsing. A useful recent data point: the $6.4 billion takeover of Onestream by Hg Capital and General Atlantic, completed in late March 2026 at approximately 8x forward ARR. Financial buyers are not retreating from software. They are getting more discriminating about which software it buys and at what price.

Private equity funds look at AI through the lens of resilience and disruption risk, not opportunity or growth. That is a meaningfully different frame from how VCs approach it. PE funds need to deliver consistent double-digit returns across a portfolio. A company that looks strong today but faces structural displacement in year three of a five-year hold is a liability, not an asset.

What makes a legacy SaaS business valuable in this environment

Given all of that, what does a PE buyer actually want to see? Based on what I am observing across active transactions, legacy tech companies are holding their value well when they have one or more of the following characteristics.

A regulatory moat:

- Accreditations, compliance certifications, and regulatory requirements create structural barriers that AI cannot simply route around. Identity providers, tax and accounting platforms, and healthcare software with regulatory certification fall into this category.

Operational complexity:

- Software that requires ongoing configuration, multi-location deployment, or continuous specialist maintenance has switching costs baked in. Customers do not leave because an alternative exists; they leave when the pain of switching is lower than the pain of staying. Complex implementations push that threshold up.

Stability-first customers:

- The customer who values predictability over novelty is a very different buyer than the engineering team chasing the latest tool. Finance departments, legal teams, regulated industries, and enterprise procurement functions tend to stay with embedded solutions. The market segment a SaaS company serves shapes its AI exposure more than its technology stack does.

AI as accelerator, not substitute:

- Bot activity prevention, fraud detection, compliance monitoring, and workflow orchestration are all areas where AI makes the existing product more valuable rather than threatening to replace it. Buyers pay premiums for this dynamic because it means AI is a tailwind, not a headwind.

Network effects and data moats:

- Platforms where the accumulated data or marketplace scale is itself the product are difficult to displace from scratch. A new AI-native entrant can build better software, but it cannot replicate ten years of proprietary customer data overnight.

For the curious, this is a SaaSpocalypse Survival Scanner that scores out how defensible your SaaS is or if it can simply be replaced by a Claude skill.

The cash flow question

There is a harder conversation that applies specifically to VC-backed companies. Cash flow is king right now. If you want to sell your company and have been running on venture fuel, you need to land the plane. That means reducing burn, prioritizing Rule of 40, reaching double-digit EBITDA margins, and demonstrating that the business can stand on its own. "Let it sink in" is a reasonable phrase for this. It takes time, and buyers are patient enough to wait for companies that are worth waiting for.

This is not a new insight, but the AI environment makes it more urgent. A VC-backed company with strong ARR growth but negative margins and unclear AI positioning is a harder sell in 2026 than it was in 2024. The combination of multiple compression and increased diligence scrutiny around AI risk means the sell-side process needs to be sharper and better prepared than it has been in recent years. I see this across every process we run right now.

AI disruption risk, the bottom line

Most SaaS founders who built something meaningful will come out fine. The adjustment required may involve adding AI where it is genuinely useful, tuning pricing if customers start pushing back, and moderating exit multiple expectations relative to the 2021 peak. But a solid exit exists for most well-run software businesses.

The companies that face real trouble are the ones that were not providing much differentiated value to begin with. AI is accelerating the exposure of that weakness, but it is not creating it. If your product was always somewhat replaceable, the market is pricing that more aggressively now. That is uncomfortable but not unfair.

For founders who want to understand clearly where their business sits on this spectrum before entering a process, reach out to the L40° team. At L40º, we work with tech and SaaS founders to help them exit their business, pressure-test positioning, frame the AI narrative credibly, and run competitive processes that capture the best available outcome in this market.

Adapted from a piece originally published on Juan Ignacio's Substack, Telefunke.